Financial statements

Financial statements are the formal summary reports of your school's financial position and performance. The system generates three standard financial statements automatically from your recorded transactions: the Trial Balance, the Income Statement (Profit & Loss), and the Balance Sheet.

These reports are typically shared with the school board, governing body, and external auditors.

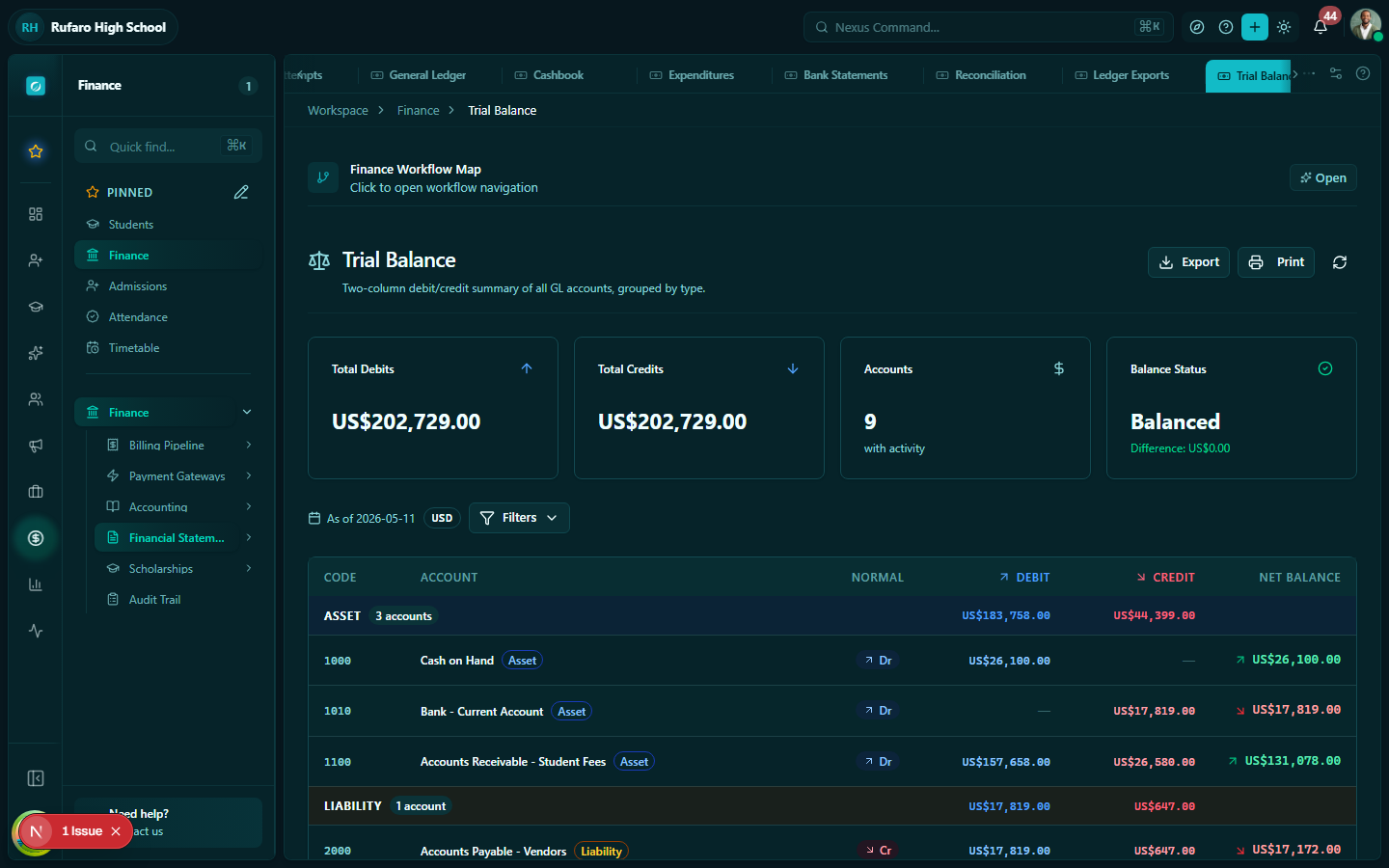

Trial Balance

Navigation: Finance → Trial Balance

The trial balance lists every account in the chart of accounts with its total debit and credit balance for a given period. The sum of all debits must equal the sum of all credits — if they don't, there is an accounting error.

Generating a trial balance

- Open Finance → Trial Balance

- Select the date range (typically a financial year or term period)

- The report is generated automatically

- Click Export to download as PDF or CSV

Reading the trial balance

| Column | Description |

|---|---|

| Account code | The GL account code |

| Account name | Description of the account |

| Opening balance | Balance at the start of the period |

| Period debits | Total debits during the period |

| Period credits | Total credits during the period |

| Closing balance | Balance at the end of the period |

The bottom rows show the grand total for debits and credits — they must match (balance). If they don't match, investigate unbalanced journal entries.

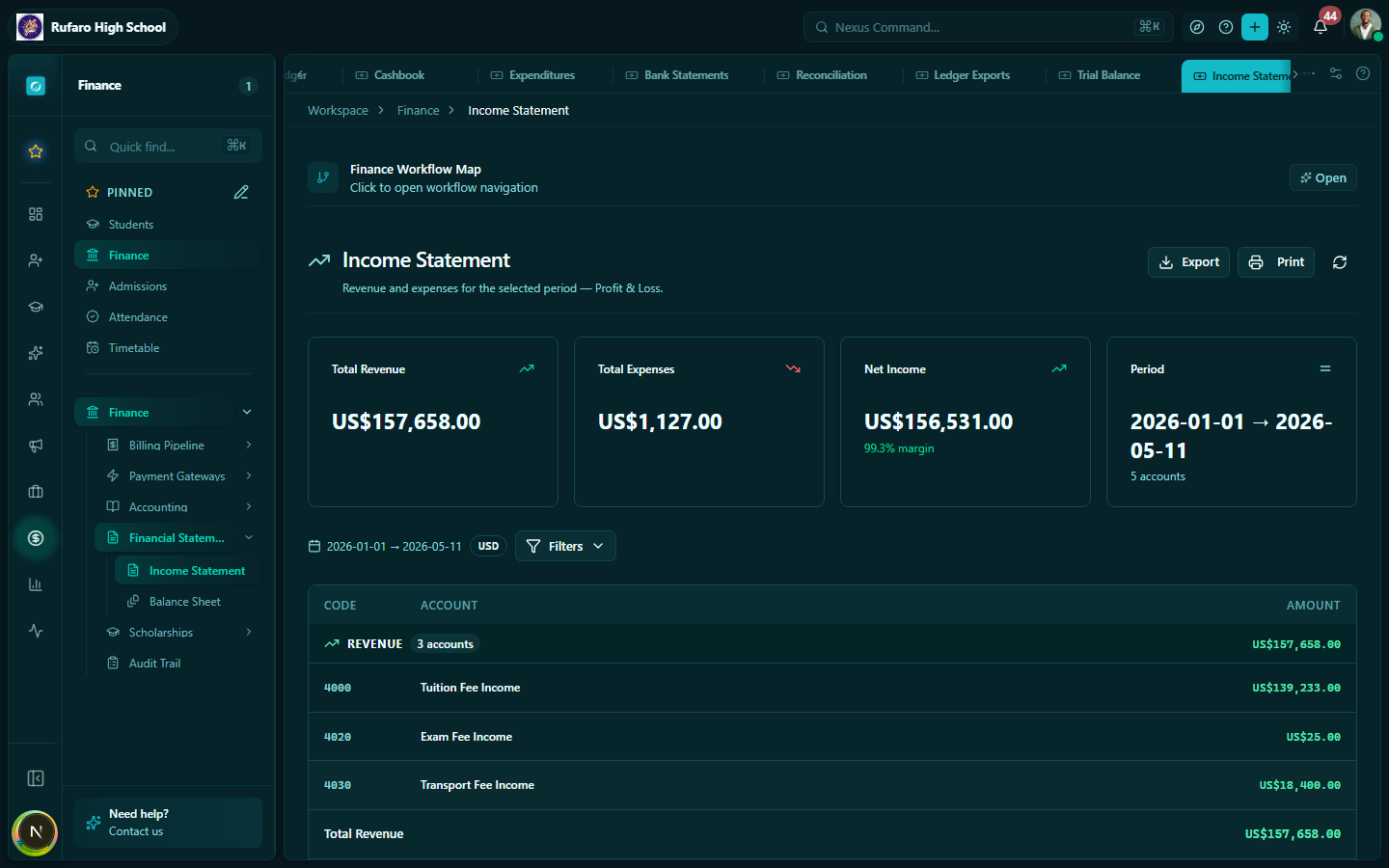

Income Statement (Profit & Loss)

Navigation: Finance → Income Statement

The income statement shows the school's revenue and expenses over a period, resulting in a surplus (profit) or deficit (loss).

Income statement structure

INCOME

Tuition income $ X,XXX

Examination fees $ XXX

Registration fees $ XXX

Other income $ XXX

─────────────────────────────────

Total income $ X,XXX

EXPENSES

Staff salaries $ X,XXX

Utilities $ XXX

Stationery & supplies $ XXX

Maintenance & repairs $ XXX

Other expenses $ XXX

─────────────────────────────────

Total expenses $ X,XXX

═════════════════════════════════

NET SURPLUS / (DEFICIT) $ XXX

Generating the income statement

- Open Finance → Income Statement

- Select the period — typically by term or full academic year

- Click Generate

- Review the figures

- Click Export PDF to produce a printable report

Comparing periods

Use the Compare toggle to see two periods side by side (e.g., Term 1 2026 vs Term 1 2025). This helps identify trends in income and spending.

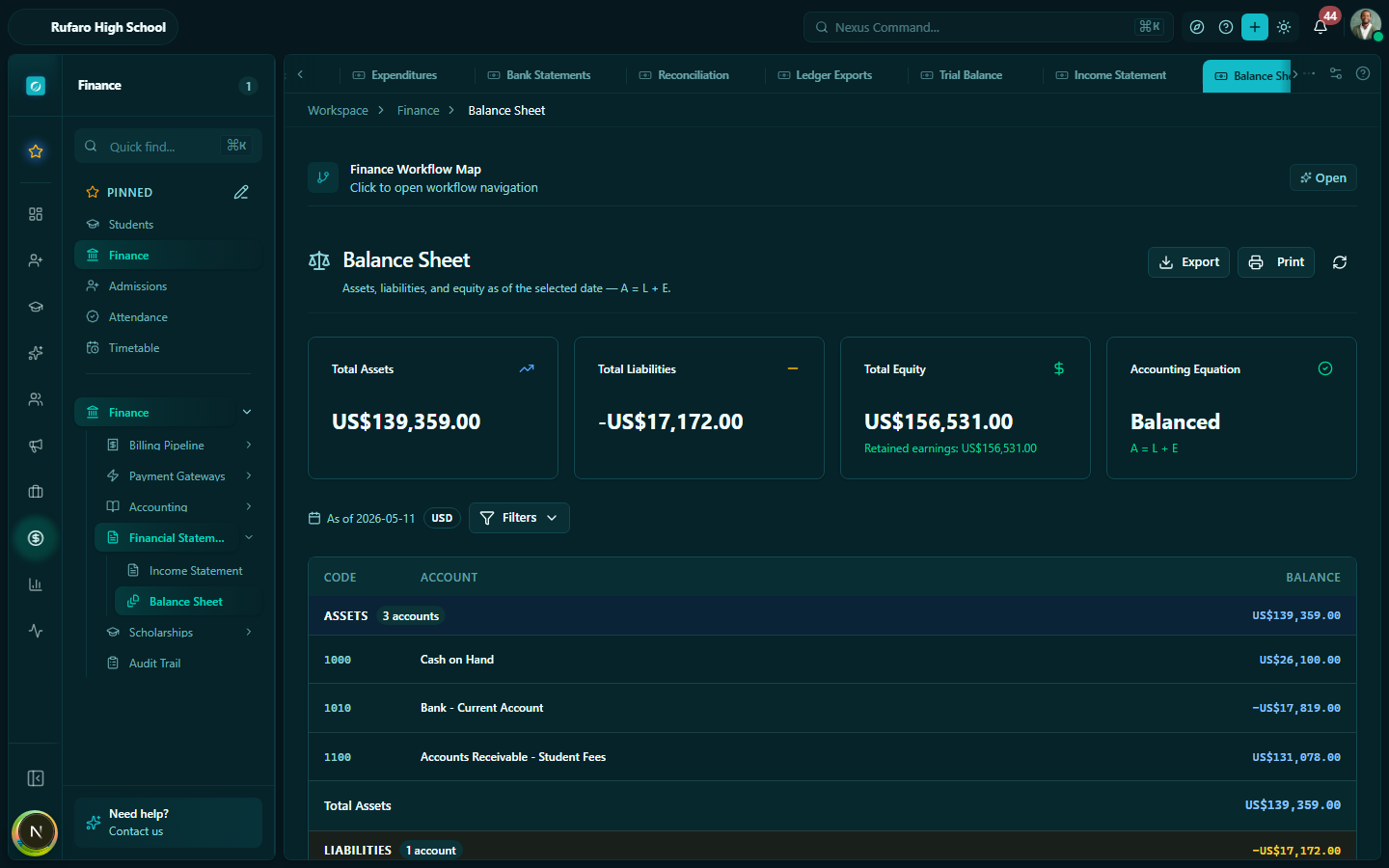

Balance Sheet

Navigation: Finance → Balance Sheet

The balance sheet shows the school's financial position at a specific point in time — what the school owns (assets), what it owes (liabilities), and its net worth (equity).

The fundamental equation:

Assets = Liabilities + Equity

Balance sheet structure

ASSETS

Current assets

Cash at bank $ X,XXX

Accounts receivable $ X,XXX ← Outstanding fees from students

Prepayments $ XXX

Fixed assets

Buildings & land $ X,XXX

Equipment $ XXX

─────────────────────────────────

Total assets $ X,XXX

LIABILITIES

Current liabilities

Accounts payable $ XXX ← Unpaid supplier invoices

Deposits received $ XXX

─────────────────────────────────

Total liabilities $ XXX

EQUITY

School fund $ X,XXX

Accumulated surplus $ XXX

─────────────────────────────────

Total equity $ X,XXX

Total liabilities + equity $ X,XXX ← Must equal Total assets

Generating the balance sheet

- Open Finance → Balance Sheet

- Select the as-at date (the date you want the snapshot for — typically the last day of a term or financial year)

- Click Generate

- Export as PDF for board reporting

Best practices for financial reporting

- Run the trial balance first at the end of each period to verify your books are balanced before producing the income statement and balance sheet

- Reconcile before reporting — complete your bank reconciliation before generating financial statements to ensure accuracy

- Export and archive statements at the end of each term and financial year — keep them as official records

- Share with the board — provide the income statement and balance sheet to the school board at each board meeting (typically end of term)

- Year-end closing — at the end of the financial year, your accountant should post a closing journal entry to transfer the net surplus/deficit to retained equity